Are you drowning in high-interest credit card debt? Feeling overwhelmed by minimum payments and accruing interest charges? A balance transfer could be your lifeline. This comprehensive guide will explain precisely how balance transfers work, helping you understand the mechanics of this potentially powerful debt management tool. We’ll explore the benefits, including the opportunity to save money on interest, and delve into the crucial considerations before transferring your credit card balance.

Understanding the intricacies of balance transfer credit cards is key to making an informed decision. We’ll cover topics such as balance transfer fees, APR (Annual Percentage Rate), and the importance of reading the fine print. Learn how to find the best balance transfer offers to suit your financial situation, and discover strategies to effectively utilize this technique to consolidate your debt and ultimately improve your credit score. Let’s demystify the process of balance transfers and empower you to take control of your finances.

What Is a Balance Transfer?

A balance transfer is a financial maneuver that allows you to move your outstanding debt from one credit card to another. This is typically done to take advantage of a lower interest rate offered by the new card, thus potentially saving you money on interest charges over time.

The process involves applying for a new credit card with a balance transfer offer. Once approved, you then authorize the new card issuer to pay off the balance from your existing credit card. The outstanding amount is then transferred to your new card, and you begin making payments on this new account.

It’s important to note that balance transfers often come with fees. These fees can vary depending on the credit card issuer and the amount transferred. There may also be a balance transfer limit, meaning you might not be able to move your entire balance. Carefully review the terms and conditions of any balance transfer offer before proceeding.

Understanding the interest rate on both your current and prospective credit cards is crucial. While a balance transfer can offer significant savings with a lower interest rate, ensure the interest rate on your new card remains lower than your current rate throughout the promotional period and beyond. Many balance transfer offers have introductory periods with low interest rates, after which the rate may increase substantially.

Effectively utilizing a balance transfer requires careful planning and discipline. To maximize savings, it’s vital to pay down the transferred balance as quickly as possible, ideally before the promotional interest rate expires. Failing to do so could negate any cost savings achieved through the transfer.

When Should You Consider One?

A balance transfer can be a powerful tool for managing your credit card debt, but it’s not always the right solution. Consider a balance transfer when you’re facing high interest rates on your existing cards and want to lower your monthly payments. This is particularly beneficial if you can find a card offering a promotional 0% APR period.

Timing is crucial. A balance transfer is most effective when you have a clear plan to pay off the balance before the promotional period ends. Otherwise, you’ll be hit with potentially high interest charges once the introductory rate expires. Careful budgeting and a commitment to consistent repayments are essential for success.

Think about your financial situation as a whole. If you’re struggling to manage your finances and consistently miss payments, a balance transfer might only offer temporary relief. Addressing the underlying spending habits is key to long-term financial health.

Finally, weigh the fees associated with balance transfers. Many cards charge a balance transfer fee, often a percentage of the amount transferred. Factor this cost into your decision and ensure the savings from reduced interest outweigh the upfront fee.

Typical Fees and Introductory Rates

Balance transfer credit cards typically charge a fee for transferring your balance from another card. This fee is usually a percentage of the amount you transfer, ranging from 3% to 5%, though some cards may charge a flat fee. It’s crucial to factor this fee into your calculations to determine whether a balance transfer is truly cost-effective.

A key attraction of balance transfer cards is their introductory APR (Annual Percentage Rate). These introductory rates are often significantly lower than the card’s standard APR, sometimes even 0% for a promotional period. This period can range from 6 to 21 months, depending on the specific card and your creditworthiness. During this promotional period, you can pay down your balance without incurring substantial interest charges, allowing you to save money on interest.

It is essential to understand that the introductory APR is temporary. Once the promotional period expires, the APR will revert to the card’s standard APR, which is usually much higher. Careful planning and budgeting are necessary to pay off as much of your balance as possible before the introductory period ends to avoid accumulating substantial interest charges.

Always carefully review the terms and conditions of any balance transfer offer, paying close attention to the fee percentage, the length of the introductory period, and the standard APR that applies after the promotional period concludes. Comparing offers from different credit card issuers is strongly recommended to find the most favorable terms.

How to Avoid Balance Transfer Traps

Balance transfers can be a powerful tool for saving money on high-interest debt, but they come with potential pitfalls. Understanding these pitfalls and how to avoid them is crucial to reaping the benefits without incurring additional fees or harming your credit score.

One major trap is the balance transfer fee. Many credit card issuers charge a percentage of the transferred balance as a fee, typically ranging from 3% to 5%. Carefully compare this fee against the potential savings from a lower interest rate over the promotional period. A high fee could negate the benefits of a lower interest rate, especially for smaller balances.

Another common trap is the limited promotional period. Balance transfer offers often come with a promotional 0% APR period, which typically lasts for a specific timeframe (e.g., 12-18 months). Failing to pay off the balance before the promotional period ends will result in a significant increase in your interest rate and substantially higher monthly payments. Accurate budgeting and a repayment plan are essential to avoid this.

Credit score impact is another critical consideration. Applying for a new credit card to obtain a balance transfer offer can temporarily lower your credit score, as it represents a new inquiry on your credit report. Additionally, consistently high credit utilization (the amount of credit you’re using compared to your total available credit) can also negatively impact your credit score. Manage your credit utilization carefully throughout the balance transfer process.

Finally, be wary of hidden fees. Some credit cards may have additional fees beyond the balance transfer fee, such as annual fees or late payment penalties. Thoroughly review the terms and conditions of any balance transfer offer before accepting it to ensure there are no unexpected charges.

By carefully considering these factors—balance transfer fees, promotional periods, credit score impacts, and hidden fees—you can effectively utilize balance transfers to your advantage and avoid common pitfalls.

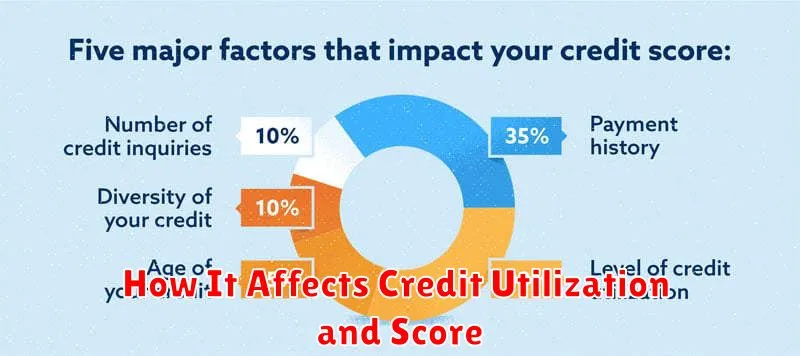

How It Affects Credit Utilization and Score

Understanding how balance transfers impact your credit utilization and score is crucial. Credit utilization refers to the percentage of your available credit you’re currently using. A lower utilization rate is generally better for your credit score.

When you perform a balance transfer, you’re essentially moving debt from one card to another. Initially, this can lower your credit utilization on the card you’re transferring the balance *from*, resulting in a potential short-term improvement in your credit score. This is because the amount of available credit remains the same, but the balance (and hence the utilization) is reduced. However, it is important to remember that this is only a temporary effect if you continue to make charges on that card.

On the receiving card, the utilization will increase. If this card already had a balance before the transfer, the impact on the credit score might be more significant. The best-case scenario is to ensure that the overall credit utilization across all your cards remains low, ideally below 30%, to avoid a negative impact on your credit score. High utilization is one of the most significant factors affecting your score.

It’s important to note that the effect on your credit score isn’t immediate. Credit bureaus update scores periodically, and the impact of a balance transfer may not be reflected immediately. Moreover, opening a new credit card to perform the balance transfer might temporarily lower your score as it can affect your average credit age.

Finally, consistently paying your balances on time, regardless of where they are, is the most important factor influencing your credit score. Timely payments outweigh the influence of credit utilization.

Best Practices to Pay Off the Transferred Amount

Successfully paying off a balance transfer requires a strategic approach. Failing to do so can negate the benefits of the lower interest rate and potentially harm your credit score.

First, create a realistic budget that incorporates the minimum payment due on your transferred balance, as well as your other financial obligations. This will help you understand how much you can comfortably allocate towards paying down the debt each month.

Next, consider a payment strategy that prioritizes paying more than the minimum payment each month. The quicker you pay off the balance, the less interest you’ll accrue. Explore options like making bi-weekly payments instead of monthly; this will effectively make an extra monthly payment each year.

Careful tracking of your payments is essential. Regularly check your credit card statement to ensure that payments are properly applied and you’re on track to meet your repayment goal. Consider using budgeting apps or spreadsheets to aid in monitoring your progress.

Finally, avoid further debt accumulation on the card with the transferred balance during the promotional period. New purchases will generally be subject to the original, higher interest rate and will hinder your progress toward paying off the transferred amount.

{kind=link}